Token Vault

PCI Audits Made Easy

TL;DR

PCI DSS compliance can cost up to $200,000 and consume months of engineering time when managed in-house, but the scope is not fixed. Tokenization through an external provider keeps cardholder data out of your systems entirely, reducing most merchants to SAQ A, the lightest possible assessment covering around 26 requirements instead of hundreds. The result is faster audits, lower costs, and engineering teams freed from compliance overhead to focus on building product.

A Collaborative Guide by PCI Proxy and usd AG.

If you're reading this, chances are you’ve felt the burden of PCI DSS compliance.

Maybe you've spent sleepless nights preparing for audits, burned through budgets to secure infrastructure, or juggled multiple teams trying to stay within scope.

You're not alone — and there is a smarter way forward.

This article is a collaboration between PCI Proxy, a leading provider of tokenization, and usd AG, a trusted PCI QSA company with decades of experience helping merchants and service providers navigate the complexities of payment security.

In this guide, you’ll gain a clear understanding of what PCI DSS scope truly involves and why reducing it is the smartest move most organizations can make.

We’ll explore practical strategies to minimize your compliance footprint, with a particular focus on how using an external tokenization provider offers one of the most effective and scalable paths to simplification.

Most importantly, you’ll see how outsourcing cardholder data handling can transform your audit experience — making it faster, cheaper, and significantly less complex.

Let’s dive in.

The Complexity of PCI DSS: A Necessary Burden

The Payment Card Industry Data Security Standard (PCI DSS) is designed to protect cardholder data — and for good reason.

Data breaches cost businesses millions, and the reputational damage can be even more severe.

But for many organizations, the road to compliance can feel overwhelming.

Achieving PCI DSS compliance is a process that can be complex, taking companies months, or even years to achieve.

Depending on your scope, it can come with over 300 requirements, covering everything from firewalls and encryption to monitoring and incident response.

And for businesses that store, process, or transmit cardholder data themselves, compliance becomes a full-time job.

A full PCI DSS Level 1 compliance journey can cost anywhere from $20,000 to over $200,000, depending on the size and complexity of your systems.

This includes everything from infrastructure upgrades and new security tools to audit fees and internal staffing.

And that’s not counting the ongoing costs to maintain compliance year after year.

In the past, companies looked to do this all in-house, which is a considerable drain on time and resources.

New staff must be recruited, or existing employees must shift their focus away from other projects.

Then the team must invest time to understand all the applicable requirements and their impact on the company’s systems, products, employees and overall infrastructure.

And since PCI DSS continuously evolves to keep pace with emerging threats, existing requirements may be updated, retired, or replaced with entirely new ones, requiring companies to stay constantly informed.

Once the requirements are understood, the team must execute the implementation, often involving system overhauls followed by an assessment.

And finally, after all of this is completed, it is time to start over again, since companies must be re-certified on an annual basis.

But what if you could dramatically reduce your scope and the number of applicable requirements?

Demystifying Scope: What’s In, What’s Out

At its core, scope refers to the cardholder data environment (CDE), which is comprised of any system, network, process, or person that stores, processes, or transmits cardholder data and/or sensitive authentication data or could impact the security of cardholder data.

The last part is often misunderstood.

It's not just where the cardholder data lives, but anything that could touch it or influence it.

To know your scope, businesses must identify, document and confirm all locations and flows where cardholder data is stored, processed or transmitted, and identify all systems that are connected to or, if compromised, could impact the cardholder data environment (for example, authentication servers, remote access servers, logging servers).

Once your scope is determined, you need to understand the different merchant or service provider levels, and the methods or processes used to assess and document compliance with PCI DSS requirements.

Levels set the who and how of validation, while SAQs and onsite audits are the methods or processes for performing that validation.

To dive deeper into the different PCI DSS levels, check out this.

Below you can find an overview of the relevant assessment types for e-commerce businesses:

The broader your PCI DSS scope, the more security requirements you must implement, monitor, and validate - and the more time and resources you’ll spend maintaining compliance.

If your organization qualifies for SAQ A, you're already operating within the lowest possible scope.

In most cases, your payment service provider (PSP) is handling cardholder data processing on your behalf in its entirety, leaving little or no room for further optimization from a scoping perspective.

However, if you're operating under SAQ A-EP or a higher category, there is likely meaningful opportunity to reduce your PCI DSS scope.

To explore how to shrink your PCI footprint without compromising security, keep reading.

Choose the Right Scope Reduction Strategy

When operating under SAQ A-EP or a higher category, the complexity and resource strain of maintaining PCI compliance is a considerable drain on time and resources and often impractical to handle entirely in-house.

But with the right scope reduction strategies, it's a strategic investment that pays dividends over time — fewer systems in scope mean fewer requirements to meet, and less risk to manage.

Scope reduction is not about cutting corners.

It’s about smart architecture and responsible delegation.

Key strategies for companies handling cardholder data include:

- Network segmentation

- Using PCI-compliant cloud providers

- Outsourcing payment processing

While all of the strategies will help to reduce the scope, none of the strategies that were just mentioned will eliminate your scope completely, nor does it remove the businesses’ responsibility for its own PCI DSS compliance.

In the next sections we will focus on tokenization, one of the most promising and effective solutions for reducing the number of applicable PCI DSS requirements in scope, if implemented correctly.

What Role Does Tokenization Play in Reducing My Scope?

The key for merchants and service providers wishing to reduce their PCI DSS scope is to not store, process, or transmit cardholder data.

If there's one tool that can achieve that, it's tokenization.

Tokenization is the process of replacing cardholder data and/or sensitive authentication data, such as a customer's Primary Account Number (PAN) or Card Verification Value (CVV/CVC), with non-sensitive placeholders known as tokens.

These tokens are randomly generated and have no meaningful value outside the tokenization system.

And unlike encryption, which is reversible with a key, tokenization is designed to be irreversible and meaningless outside the tokenization service.

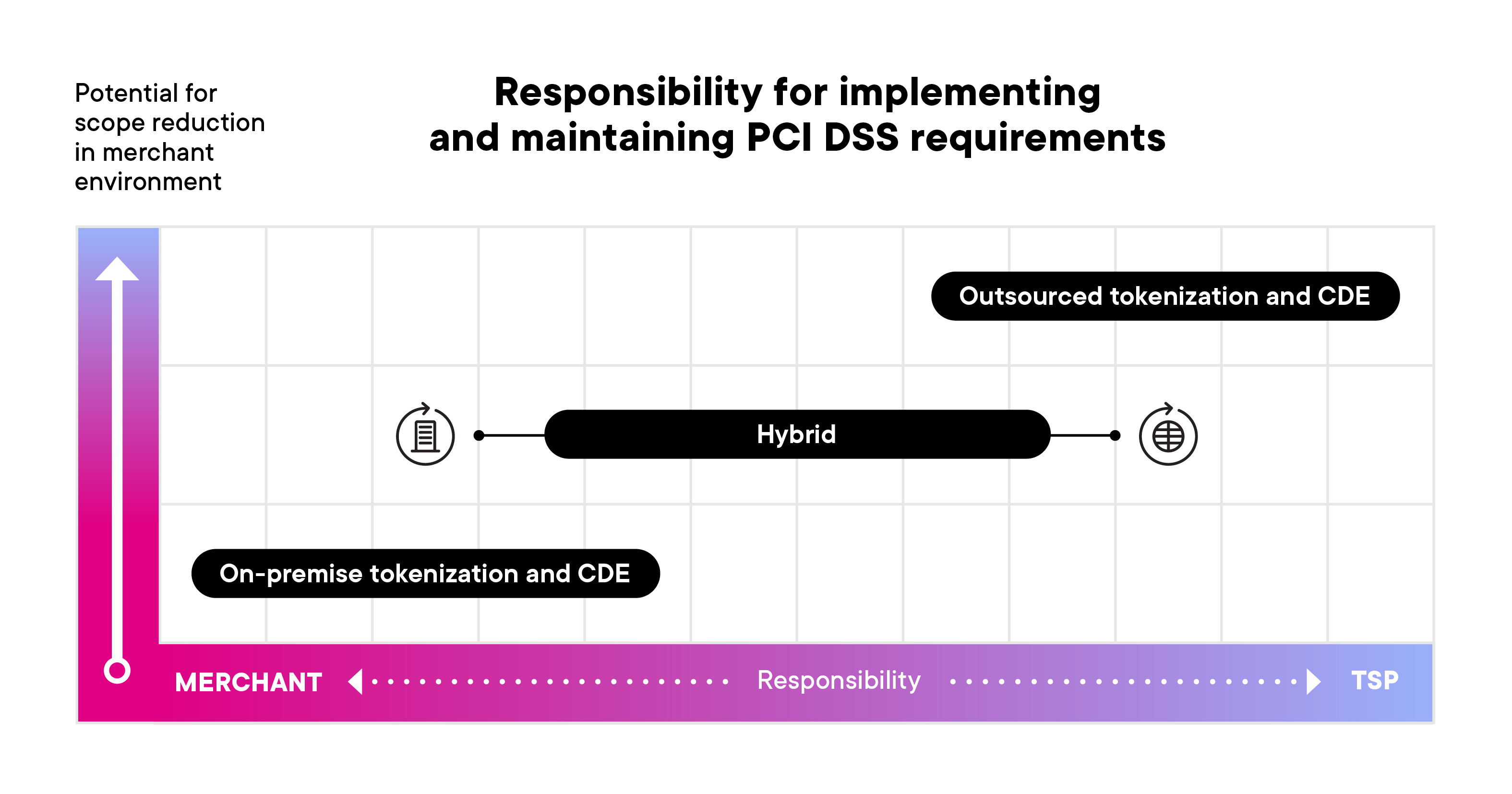

Building tokenization internally means sensitive cardholder data must enter your systems before it can be tokenized.

As a result, your environment remains in PCI DSS scope and must meet all relevant security and compliance requirements.

By contrast, outsourcing tokenization to a tokenization service provider — depending on how it’s implemented — can significantly reduce scope, and in some cases, nearly eliminate it.

Here's why: PCI DSS allows businesses to limit their compliance scope and obligations if they do not store, process, or transmit cardholder data themselves.

So, when a merchant or service provider leverages tokenization, their environment interacts only with tokens, which are not considered as sensitive anymore.

This outsourcing effectively removes cardholder data from their systems, shrinking the scope of your PCI DSS assessment.

For merchants, this reduced scope often aligns with the SAQ A, the shortest and least burdensome PCI DSS assessment.

Even Level 1 merchants — those processing over 6 million transactions annually — can benefit from this approach.

While Level 1 merchants are typically required to undergo a Report on Compliance (ROC) conducted by a Qualified Security Assessor (QSA), the ROC’s scope can be limited to the minimal set of controls applicable to an SAQ A environment, typically around 26 requirements in PCI DSS v4.0.1, while the remaining requirements are considered as not applicable.

Similar procedure applies to service providers.

Although service providers are typically not allowed to complete an SAQ A as this is only intended for merchant entities, their SAQ D scope can still be limited to a minimal set of controls applicable as the majority of requirements are not considered to be applicable anymore — streamlining compliance and cutting down on associated costs and complexity.

Universal Token Vaults: How It Minimizes Your Compliance Workload

If your cardholder data environment (CDE) qualifies for an SAQ A-EP or a higher category, you are likely to have opportunities to reduce your PCI DSS scope — and using a tokenization service provider is often a key part of that strategy.

The reason universal token vaults have such a powerful impact on a merchant’s or service provider’s PCI DSS environment is simple: they keep cardholder data out of your systems entirely.

How? By offering interfaces and APIs that tokenize sensitive cardholder data before it ever enters your environment and de-tokenize it when it leaves your environment.

Because your systems never store, process, or transmit cardholder data, your PCI DSS scope can be reduced to the absolute minimum.

Instead of undergoing a time-consuming and costly onsite assessment or navigating the complexity of an SAQ D or SAQ A-EP in its entirety, many merchants and service providers are now eligible for a reduced and streamlined assessment — a so-called partial assessment referring to SAQ A, for example.

This limited assessment focuses primarily on confirming that you are correctly outsourcing the processing and securing access to a tokenization service provider.

Fewer systems for your QSA to evaluate, no cardholder data environments to secure, and significantly fewer technical controls to implement, monitor, and prove.

As a result, businesses that make the shift often find that compliance is no longer a year-round struggle, but a lightweight, annual validation.

And for your QSA, the audit becomes less about probing every system and more about verifying how the outsourced services are integrated, what contracts are in place, and how access is controlled.

And importantly, outsourcing doesn’t mean giving up control — it means focusing your resources where they matter most.

The Benefits in a Nutshell

Outsourcing payment processing and using tokenization through a certified third-party provider such as PCI Proxy isn't just a tactical shortcut — it's a strategic move with tangible, cross-functional benefits:

- Minimal PCI Scope: With no cardholder data in your environment, most businesses qualify for a partial assessment scope, significantly reducing compliance efforts.

- Stronger Security: By removing sensitive data entirely, you reduce the risk of breaches, eliminate the need for encryption and key management, and ensure data protection is handled by experts.

- Faster, Lighter Audits: With fewer systems in scope, audits become quicker and less disruptive — often completed with minimal QSA involvement.

- Operational Efficiency: Developers no longer need to architect PCI DSS, freeing up time and resources. Infrastructure teams can focus on business-critical systems.

- Scalable Payment Flexibility: Tokens can be safely used across systems and integrations, enabling consistent experience without reintroducing cardholder data risk.

- Lower Costs: No need to hire dedicated security teams or build infrastructure from scratch.

- Customer Trust: Demonstrating a modern, secure payment infrastructure can be a competitive advantage.

In short, by removing what you don’t need to carry — cardholder data — you simplify compliance, reduce risk, and reclaim focus on what matters most: growing your business.

Audits Made Easy: A QSA’s Perspective

The first thing many businesses ask after integrating with a token service provider is: What does this mean for our next audit?

To get an initial understanding of how PCI DSS assessments are structured and conducted, this article by usd AG offers a clear walkthrough of the entire process—from initial scoping to final reporting.

It outlines the role of the QSA, key phases of the assessment, and how organizations can prepare effectively to ensure a smooth and successful audit.

When implemented correctly and by adopting a robust tokenization solution, organizations effectively remove the cardholder data from their environments.

This architectural shift doesn't just reduce risk; it fundamentally alters the audit dynamic.

By removing cardholder data from your environment and replacing it with tokens, you effectively limit the systems that need to be assessed.

As a result, your QSA can often shift from examining hundreds of technical controls across your entire infrastructure to focusing on a core set of requirements, including but not limited to:

- Secure integration of tokenization solution

- Identity & access management

- Regular ASV scans

- Information security governance incl. TPSPs oversight

In real-world assessments, businesses go from multi-month resource-draining audits to streamlined evaluations that are completed in a fraction of the time.

Tokenization also makes it easier for teams to demonstrate control effectiveness, as the reduced scope allows for better focus, clearer documentation, and fewer edge cases to explain.

In short, tokenization isn't just a technical implementation — it's a strategic decision that reshapes how compliance is managed.

The result? Audits transform from annual disruptions into lightweight validations that preserve resources while enhancing security posture.

Final Thoughts

PCI DSS compliance can feel like a moving target — complex, time-consuming, and resource-intensive.

But it doesn’t have to be.

As this guide has shown, reducing your PCI scope through smart delegation and proven technologies like tokenization is not only possible, it’s increasingly essential.

By removing sensitive cardholder data from your environment, you shift the narrative: from reactive audits and constant firefighting to a streamlined, proactive approach that enhances security and supports growth.

You reduce the burden on your teams, speed up audit processes, and gain the confidence that your systems are designed with long-term resilience in mind.

Simplifying compliance isn’t about doing less — it’s about doing it smarter.

And with the right partners by your side, compliance can become less of a barrier and more of an enabler.

Let’s Continue the Conversation

Every business is different — and so is every compliance journey.

Whether you’re a fintech scaling globally, a SaaS provider building out new payment capabilities, or an enterprise looking to modernize legacy infrastructure, PCI Proxy can help you reduce scope, minimize audit fatigue, and get back to building.

If you’re ready to take the complexity out of PCI DSS, our team is here to support you every step of the way — from architectural review to hands-on implementation guidance.

Find out more: www.pci-proxy.com

About usd AG

usd AG protects companies against hackers and criminals.

More security is its mission.

Its work is as dynamic and diverse as the threat itself.

As an accredited assessor, usd AG advises and certifies companies worldwide according to the specifications of the credit card industry and other international IT security standards.

The experts at usd HeroLab identify vulnerabilities in IT systems and applications. usd security consultants advise companies holistically on questions of information security, risk management, and IT compliance.

The Cyber Security Transformation Academy (CST Academy) promotes exchange and knowledge transfer within the community.

Since 2004, usd AG has been an accredited assessor by the PCI Security Standards Council (PCI SSC), authorized to operate across all relevant Payment Card Industry standards.

Their PCI experts support over 200 companies worldwide — precisely where their expertise is needed: from ASV scans and consulting to comprehensive assessments.

As a strategic partner to the PCI SSC Global Executive Assessor Roundtable (GEAR) they also support the PCI Security Standards Council as one of 20 companies worldwide with their knowledge from thousands of PCI projects.

Find out more: www.usd.de/en

About PCI Proxy

Today’s most advanced companies use PCI Proxy to tokenize and store sensitive payment data because achieving PCI compliance shouldn’t take ages, slow down product sprints, or cost a fortune.

We built PCI Proxy to reduce the cost, risk, and complexity of PCI compliance — so you can focus on building great products, not navigating regulations.

Find out more: www.pci-proxy.com